Fraud strategy: a Bank’s secret weapon for acquisition and retention

Fraud strategy: a Bank’s secret weapon for acquisition and retention

James Roche, a principal fraud consultant at FICO, discusses the findings of recent research into fraud, identity and digital banking, and the opportunities for banks to improve customer experiences

Investing in fraud departments and robust fraud prevention strategies has often been viewed as an important yet inconvenient overhead. However, new consumer research has demonstrated the value of fraud protection as a key brand value. More than one in three consumers seeking a new financial account ranked good fraud protection as their top consideration when opening a new account; 73% of respondents placed fraud prevention within their top three priorities. Yet, underlining the careful balancing act financial institutions must achieve in protecting their customers and their own business without creating unwelcome friction, almost one in five of the 1,000 UK consumers surveyed also said they would abandon an application if ID checks took too long.

Fast, friction-free fraud prevention has to be the ultimate goal for financial services providers. And, done well, it can actually deliver significant benefits.

Holistic benefits of good fraud prevention

With consumers clearly expecting their financial services providers to have robust strategies in place, institutions can actually use fraud protection as a competitive advantage. They can highlight their strategies in marketing messages as long as they also ensure application and onboarding processes – protections, fraud checks and ID proofing – are appropriate, proportionate and time-efficient.

While 34% of the consumers surveyed said they are more likely to open a financial account digitally than they were a year ago, the expectation for a frictionless experience has also increased. The expectation is for the application process to be fast. Almost one in five said they would abandon an application if the checks are too difficult or take too long. Two thirds expect to spend less than 30 minutes opening a current account.

Forensic analysis

With good analysis, FIs can identify if there is one place in the onboarding process that sees a high proportion of dropouts. Changes can then be made to boost success. Perhaps altering the order in which checks are made and assessing whether some checks could happen once the customer has been accepted, for example. In addition, institutions could consider looking into two-way, conversational, and automated communications that help applicants to overcome any difficulties and encourage them to complete their application.

The growth of biometrics

The other factor that is shifting the fraud prevention landscape is how technology advances – and consumer acceptance of them – has changed when it comes to identity verification.

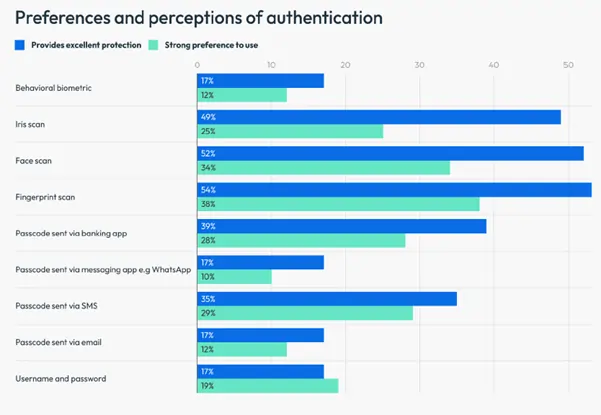

Just a few years ago biometrics was an unknown science for consumers. The new research shows the shift, with 54% believing fingerprint scans provide essential protection; 52% ranked face scans and 49% iris scans. However, more education is still needed on behavioural biometrics, as just 17% believe these provide ‘excellent’ protection.

Security concerns

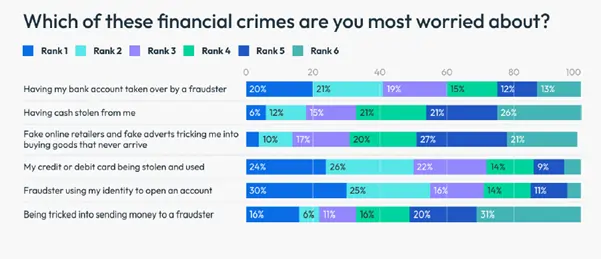

The research also identified the financial crimes that consumers are most worried about, with identity theft to open a new account ranked top at 30%.

Respondents are less worried about fraud that falls outside of the direct banking system, such as theft of cash and shopping scams. Given the headlines about people losing large sums to scams, it’s notable that they are significantly less worried about being tricked into sending money to a fraudster with just 16% selecting this as their top fear. Bank account takeover was ranked the crime most feared by 20% of respondents, meaning it is crucial that institutions can give customers confidence that they use the best processes to mitigate against these threats.

Balancing security with simplicity

Financial institutions must manage different fraud types across the customer lifecycle, with each having the potential to taint the customer experience. Taking an enterprise fraud approach that incorporates all fraud types and works across different portfolios and channels means organisations can put the customer at the heart of fraud strategies. By breaking down siloes and sharing data, financial institutions can achieve better outcomes that lower fraud losses and improve customer experience.

Aiming for completely frictionless experiences could leave a financial institution over-exposed to fraud. Indeed, as the research identified, appropriate friction can actually help customers feel protected. Checks must be proportionate and personal to each customer and interaction. Therefore, fraud protection needs to be adaptive, using all streams of customer data and identity solutions working together with centralised decision-making for the best outcome for the customer and the institution.

(1) Research conducted online by an independent research company adhering to research industry standards. 1,000 UK adults were surveyed, concluding in November 2023.